money manifestation

Wealth Identity: Build It Before You Spend

Wealth identity grows when your future-self story becomes familiar before your card comes out. Use short daily audio to choose money with a steadier self.

A receipt sits in your bag. Your wallet is still warm from your hand. Wealth identity means becoming the kind of person who can pause before buying, earning, saving, or asking. Future-self audio helps because it lets you hear that person first, before spending tries to speak for you.

What is wealth identity, really?

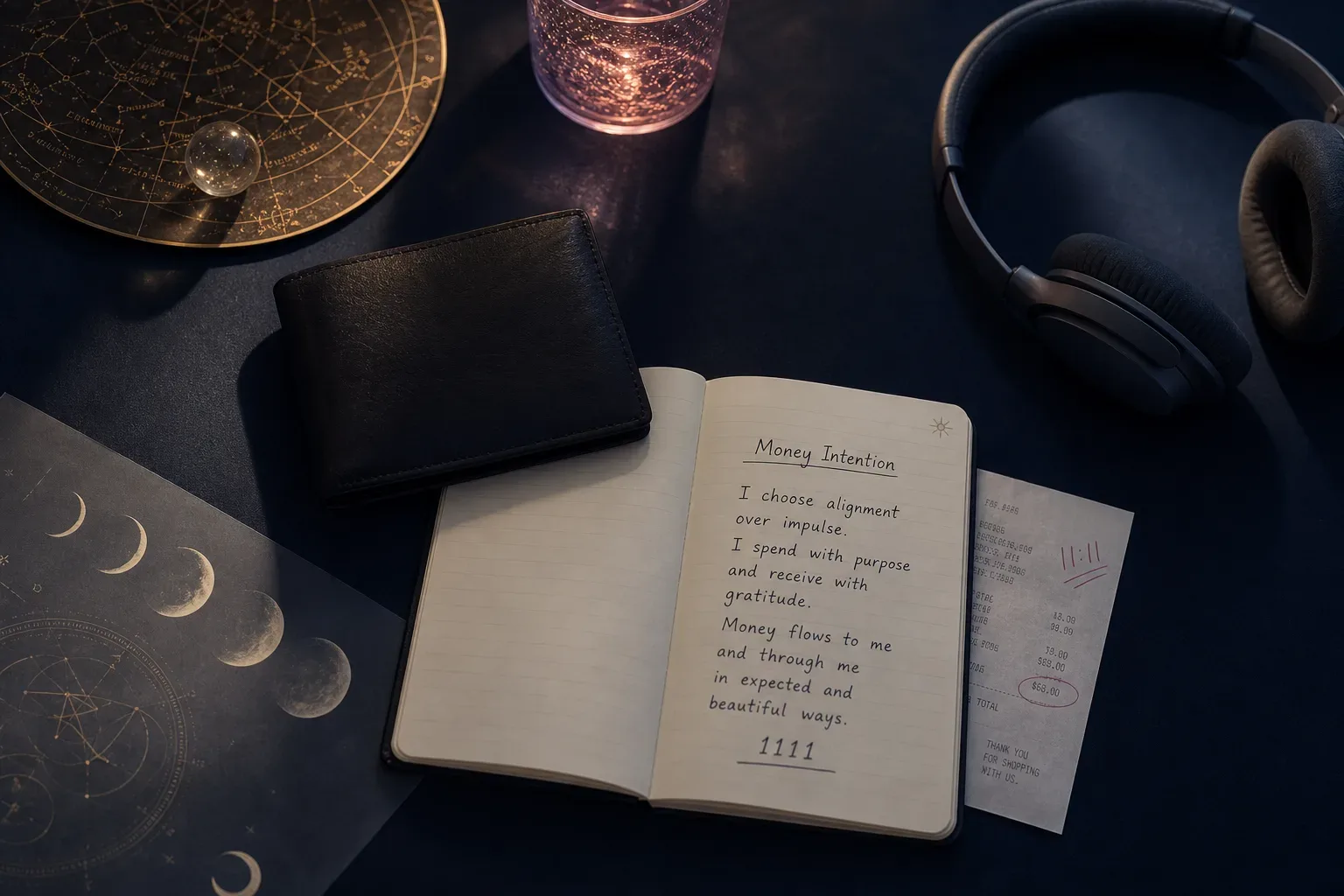

Wealth identity is the money self you practice until your choices begin to recognize you.

It’s not a mood board with expensive chairs. Though, as a vision-board purist, I respect a chair that knows who it is. Wealth identity is quieter. It’s the story your nervous system believes about what money means, what you’re allowed to keep, what you must prove, and what happens when you have more than enough for today.

The Federal Reserve’s 2023 report on household well-being found that 63% of U.S. adults said they could cover a $400 emergency expense using cash or its equivalent. That means 37% would need another route. That number matters because identity is often built under pressure. If money has mostly appeared as pressure, the self you bring to money may expect tension even when the numbers improve.

You can see wealth identity in tiny moments:

- You get paid and feel the urge to spend before the money can settle.

- You want to raise your rate, then hear an old sentence in your head.

- You save for three weeks, then break the pattern after one hard day.

- You buy something to feel like the future has already arrived.

Wealth identity is not pretending you’re wealthy. It’s practicing the behavior of someone who no longer needs money to prove safety in the next five minutes.

This sits inside the larger practice of manifestation, but it stays close to real life. Neville Goddard wrote often about living from the wish fulfilled. Joe Dispenza speaks about rehearsing a new self until the body knows it. You don’t have to copy their language. You can simply ask: if money were no longer the loudest proof of who I am, what would I do next?

Why build wealth identity before spending?

You build it before spending because the moment before a purchase is where identity either leads or follows.

Spending is fast now. A 2024 Pew Research Center report noted that roughly three-quarters of U.S. adults had bought something online using a phone. That’s not bad. It’s just frictionless. When friction disappears, identity has to become the pause. Otherwise the old self can make a decision in three taps and call it destiny.

Behavioral economist Richard Thaler’s work on mental accounting, first formalized in the 1980s, showed that people treat money differently depending on its category. A tax refund feels different from a paycheck. A cash gift feels different from rent money. Your wealth identity is another kind of account. It tells you which self is allowed to touch the money.

Here’s the quiet comparison:

| Before spending from fear | Before spending from wealth identity |

|---|---|

| “I deserve this because I’m tired.” | “I can care for myself without erasing tomorrow.” |

| “If I don’t buy it now, I’ll miss out.” | “If it’s true for me, it can survive a pause.” |

| “This proves I’m doing well.” | “My choices don’t need to perform.” |

| “I’ll fix the numbers later.” | “I look before I agree.” |

Implementation-intention research from Peter Gollwitzer, cited widely since 1999, found that if-then plans can improve follow-through because the cue is decided ahead of time. Wealth identity works the same way when it’s specific. Not “I’m good with money.” More like: “When I want to buy from panic, I listen first.”

Affirmations can support this, but they’re not the whole practice here. A sentence can steady you. Audio can place you inside the sentence long enough to hear yourself believe it.

How does future-self audio change the money decision?

Future-self audio gives your brain and body a remembered version of you to return to before the old pattern takes the chair.

The the AYA Method is a daily audio manifestation practice. Each day you listen to a short personalized recording — your Dream-Self Moment — narrated from the version of you who has already manifested the life you intend. Listening is the practice. Repetition is the work. The audio is the method.

That matters for wealth identity because money choices are rarely just math. They’re memory, status, family scripts, fear, hope, and the little ache of wanting to feel different by Friday. In the American Psychological Association’s 2023 Stress in America survey, money was named as a significant source of stress by 63% of adults. When stress is high, your choices often narrow. You reach for relief, not truth.

Future-self audio widens the room. It lets you hear the version of yourself who pays the invoice calmly, waits 24 hours before buying, asks for the better fee, or lets the cart sit there without turning it into a moral trial. Hal Hershfield’s future-self continuity research, including studies published in the Journal of Marketing Research in 2011, found that people who feel more connected to their future self tend to make more future-minded financial choices.

A simple audio practice can be built like this:

- Choose one money moment that keeps repeating.

- Write the scene in present tense, from the future self who has changed it.

- Keep the recording between 2 and 4 minutes.

- Use sensory details: the table, the bank app, the breath before you answer.

- Listen once daily, and again before the trigger.

The voice you rehearse becomes the voice that arrives first.

What should your wealth identity audio actually say?

Your audio should describe a specific money self in a specific scene, using plain words you can believe today.

Don’t start with numbers if numbers make you freeze. Start with posture. “I look at my account without flinching.” “I wait before I buy.” “I ask for the rate with a steady voice.” “I let money stay.” These are small sentences, but small is useful. BJ Fogg’s behavior work at Stanford, published for a broad audience in 2020, argues that tiny behaviors are easier to repeat because they require less motivation.

Try this structure for a two-minute recording:

- Arrival: “I’m standing in my kitchen. The morning is quiet. I know what’s in my account.”

- Identity: “I’m someone who lets money be seen. I don’t hide from numbers.”

- Choice: “Before I buy, I listen. I ask whether this supports the life I’m already building.”

- Proof: “Yesterday I waited. Last week I saved. Today I ask clearly.”

- Close: “I can want things without being ruled by wanting.”

Notice the scale. No grand speech. No glittering fantasy. The Journal of Behavioral Medicine has published many small studies on self-regulation practices, and the consistent theme is not drama. It’s repetition, attention, and a cue you can return to. Dr. Andrew Huberman often says, in his public teaching on learning and neuroplasticity, that attention and repeated action are part of how the nervous system changes.

If you use the AYA app, the Dream-Self Moment carries this for you as audio. The app also includes a daily affirmation and a Manifestation Board as complements. They can help you see and name the intention. But for this practice, listening comes first.

A rich life is not proven by a rushed purchase. It’s proven by the self who can wait and still feel whole.

How do you practice for seven days before you spend differently?

Practice for seven days by pairing the same audio with one repeating money cue and one visible proof.

Seven days won’t rewrite every pattern. It will give you enough evidence to stop calling the new self imaginary. The European Journal of Social Psychology published a 2009 habit-formation study by Phillippa Lally and colleagues showing that automaticity can take a median of 66 days, with wide variation. So think of seven days as a beginning sample, not a finish line.

Here’s a clear week:

- Day 1: Name the leak. Choose one pattern: late-night shopping, undercharging, avoiding your balance, saying yes to plans you can’t afford.

- Day 2: Record the future-self scene. Keep it under 4 minutes.

- Day 3: Listen before the cue. Not after. Before.

- Day 4: Add one sentence of proof. “I checked the number.” “I waited.” “I asked.”

- Day 5: Remove one frictionless temptation. Delete one saved card, unsubscribe from one sales list, move one app.

- Day 6: Make one clean money choice. Save, pay, ask, decline, or buy without fog.

- Day 7: Read the proof aloud. Let your body hear the evidence.

If timing matters to you, you might place this beside your own ritual calendar. Some readers like to pair intention work with lunar dates or birth-chart timing; astrology and manifestation can give that practice a frame. Just don’t let timing replace listening. The audio is still the method.

The Consumer Financial Protection Bureau has reported for years that automatic payments and reminders can reduce missed bills for many households. That’s the practical cousin of this work. You’re not waiting for a mood. You’re building a cue.

How do you know your wealth identity is becoming real?

You know it’s becoming real when your smallest money choices start matching the self you’ve been hearing.

Look for behavior before emotion. Feeling steady is lovely. Acting steady while still nervous is cleaner proof. A 2016 Psychological Bulletin meta-analysis led by Benjamin Harkin found that monitoring progress toward goals improves the chance of success, especially when the monitoring is recorded or public. You don’t need public tracking here. Private truth is enough.

Use three measures for 14 days:

- Pause count: How many times did you listen before spending or asking?

- Proof count: How many choices matched the recording?

- Repair count: How many times did you return after slipping?

Repair count matters. The old self will still visit. She may bring a discount code. She may whisper that one purchase will make the whole week feel less jagged. You don’t need to hate her. She was trying to help with the tools she had.

You can also connect this practice back to manifestation when you need a wider frame, and to affirmations when you need one sentence to carry into the day. But don’t confuse support with the center. For wealth identity, the center is the moment you hear your future self before money moves.

There’s an old podcast habit I love: before an interview, I write one line at the top of the page. Not a goal. A way of being. “Listen longer than you perform.” Money can be met the same way.

The future self doesn’t arrive with noise. She arrives as the next honest choice.

Keep the voice close. Let the receipt stay quiet.